Personal Finance & Lifestyle Design

“The goal of life is not to accumulate wealth but to have enough — and to know when enough is enough.” — John C. Bogle, Enough

The Story

An American businessman is on vacation in a small coastal village in Mexico. He is the kind of man who is never really on vacation — his phone is nearby, his mind is half elsewhere, and he has already mentally drafted two emails he plans to send when he gets back to the hotel.

Walking along the dock one afternoon, he notices a small fishing boat arriving at the pier. Inside is a Mexican fisherman with several large yellowfin tuna. The businessman, impressed, strikes up a conversation.

“Great catch,” he says. “How long did it take you?”

“Not long,” the fisherman replies. “A few hours.”

“Why didn’t you stay out longer and catch more?”

The fisherman shrugs. “I have enough. This will feed my family and leave some to sell.”

The businessman frowns. “But what do you do with the rest of your day?”

“I sleep late. I fish a little. I play with my children. In the evening I walk to the village, drink wine with my friends, play guitar. I have a full life.”

The businessman can barely contain himself. He leans forward.

“Listen — I have an MBA from Harvard. I can help you. You should fish longer every day. In a few weeks you’ll have enough money to buy a second boat. With two boats, in a few months you can buy a third. Eventually you’d have a fleet. Instead of selling to a middleman, you could negotiate directly with the processing plants — or even open your own. Then you move to Mexico City. Then Los Angeles. Then New York, where you’d run your multinational fishing empire.”

The fisherman looks at him. “And how long would all this take?”

“Fifteen, maybe twenty years.”

“And then what?”

The businessman grins. “Then you retire. You move to a small coastal village. You sleep late. You fish a little. You play with your grandchildren. In the evening you drink wine with your friends and play guitar.”

A long pause.

The fisherman smiles and walks home.

The Parable’s Power — and Its Limits

If you’ve spent any time in personal finance circles, you’ve probably encountered this story before. It has been quoted in Tim Ferriss’s The 4-Hour Workweek, circulated in thousands of blog posts, printed on motivational posters, and shared at dinner parties as an argument against ambition, corporate culture, and the relentless pursuit of more.

It is a beautiful story. And like all beautiful stories, it contains a truth that is real, a truth that is incomplete, and an assumption that most people never examine.

Let’s take all three seriously — because the fisherman’s story, properly understood, is not a simple argument against wealth-building. It is an argument for something more specific and more useful: defining your finish line before you start the race.

The Businessman’s Steelman: Is He Actually Right?

Before we canonize the fisherman, let’s be honest about what his life doesn’t have.

No safety net. The fisherman’s contentment depends on the fish continuing to bite, his health remaining good, the boat not needing expensive repairs, and no unexpected emergency arriving — a sick child, a drought, a storm that wrecks the boat. He is one bad season away from hardship. One medical crisis away from catastrophe.

The businessman’s plan — as ridiculous as the circular logic makes it look — is partly about building resilience. Wealth is not just a number. It is optionality. It is the ability to absorb shocks without having your life collapse. The fisherman’s simple life is deeply vulnerable to exactly the kinds of unpredictable disasters that money defends against.

No leverage for anyone else. The fisherman feeds his family. That is genuinely good. But the businessman’s fleet — if he built it — would employ dozens of people, feed hundreds of families, and create economic activity in his community. The parable treats ambition as purely self-serving, but at scale, productive enterprise creates value that extends far beyond the entrepreneur.

The assumption of contentment. The parable works because the fisherman is already content. But many people aren’t. Many people have genuine ambitions beyond leisure — they want to build things, solve problems, create art, fund causes, leave legacies. The fisherman’s life would be a prison for them. The parable doesn’t acknowledge that “enough” is not the same for everyone, and that for some people, the drive to build is itself a source of meaning, not just a means to an end.

The businessman is not simply wrong. His error is not ambition. His error is assuming that the fisherman shares his values — and that the goal of the fisherman’s life should be to arrive, via a twenty-year detour, at what he already has.

The Fisherman’s Steelman: The Hidden Cost of “More”

But the fisherman is pointing at something real that the businessman cannot see.

Lifestyle inflation is a treadmill, not a ladder. The businessman’s plan requires the fisherman to spend twenty years living differently than he wants to live — working harder, stressing more, sacrificing time with his children — in order to eventually return to what he already has. This is only rational if the endpoint is meaningfully different from the starting point. But the parable reveals it isn’t.

This is the hedonic treadmill made visible: the assumption that more money will bring more happiness, when the research — and the fisherman’s own life — suggests that beyond a basic level of comfort and security, additional wealth produces diminishing returns on wellbeing.

Time is the scarcest resource. The businessman talks about money as though it is the primary constraint. But the fisherman is already spending his time on the things that matter to him — his children, his friends, his music, his fishing. The businessman’s plan asks him to spend twenty years on things that don’t matter to him, in exchange for the right to do what he’s already doing.

You cannot buy back the years you worked when you didn’t want to. You cannot invest your way back to your children’s childhoods. Time spent is the one genuinely non-renewable resource in human life, and the fisherman — intuitively, without an MBA — seems to understand this more clearly than his advisor.

The finish line keeps moving. The businessman says fifteen or twenty years. But we know, from watching real lives, that it rarely works that way. The man who plans to retire at 50 after building his empire discovers at 50 that he needs just a little more security, that the business can’t run without him, that the market shifted and he lost some ground. The goalposts move. The enough-point recedes. Twenty years becomes thirty, and then the window with the children is closed and the guitar stays in its case.

The fisherman’s wisdom is not that ambition is bad. It is that a life deferred is not a life banked. You cannot save up unlived experiences for later withdrawal.

The Concept of “Enough” — The Question Nobody Asks

Here is the most important financial question most people never ask:

How much is enough for me?

Not “how much can I accumulate?” Not “how much do my peers have?” Not “how much would make me feel secure?” But specifically, concretely: what annual income, what portfolio size, what lifestyle would constitute — for me, given my actual values — a genuinely good life?

John Bogle wrote an entire book called Enough — inspired by a conversation at a party between Kurt Vonnegut and Joseph Heller. Vonnegut pointed out that their host, a hedge fund manager, had made more money in a single day than Heller had earned from Catch-22 in its entire history. Heller responded: “Yes, but I have something he will never have. Enough.”

The concept of “enough” is almost radical in a culture that treats accumulation as an end in itself. Financial media, advertising, and social comparison all push in the same direction: more is better, and you don’t have enough yet. The fisherman rejects this premise entirely. He has defined his enough — freshly, clearly, without ambiguity — and he is living it.

Most people never define it. They move through their financial lives with a vague sense that they need “more,” pursuing a target that shifts every time they approach it. They upgrade their lifestyle with every raise, which upgrades their “enough” target, which requires another raise, which generates another upgrade. The treadmill spins. The destination never arrives.

The most important financial exercise you can do is not calculating your investment returns. It is defining your enough.

Your Personal Freedom Number

Here is a concrete way to do it.

Step 1: Define your ideal annual spending. Not your current spending — your ideal spending. If money were not the constraint, what would your life cost per year? Include housing, food, travel, hobbies, healthcare, giving, and everything else that matters to you. Be honest. Don’t artificially inflate it with fantasy luxuries you don’t actually want, and don’t artificially deflate it to seem virtuous.

Call this number S.

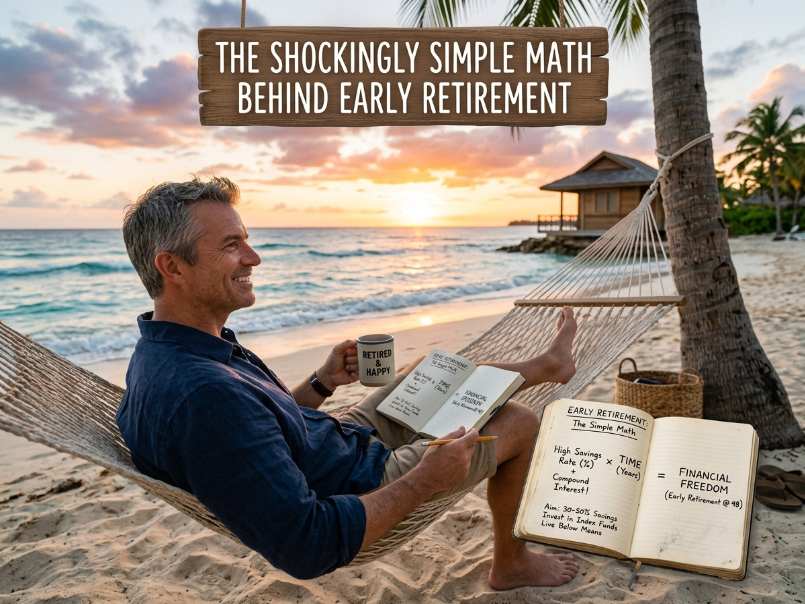

Step 2: Calculate your freedom number. Using the 4% safe withdrawal rate — the rate at which a diversified investment portfolio has historically sustained 30+ years of withdrawals — your freedom number is simply:

Freedom Number = S × 25

If your ideal annual spending is $50,000, your freedom number is $1,250,000. If it’s $80,000, your freedom number is $2,000,000. If it’s $40,000, your freedom number is $1,000,000.

Step 3: Calculate your current savings rate and project your timeline. Using the savings rate table from Article #1 of this series, estimate how many years at your current savings rate it will take to reach your freedom number — assuming roughly 7% real returns on a diversified index fund portfolio.

Step 4: Ask the real question. Is the gap between now and your freedom number worth the trade — the years of continued work, the deferred choices, the lifestyle you’re holding back?

For some people, the answer will be yes. They enjoy their work. The timeline is short. The gap is manageable. For others, the answer will be no — and the right response is to dramatically reduce spending, which simultaneously reduces the freedom number and accelerates the timeline.

The point is not to arrive at a specific answer. The point is to ask the question deliberately, with real numbers, rather than drifting through decades of accumulation toward a finish line you’ve never actually drawn.

The Thing the Parable Gets Right

The fisherman is not making an argument against wealth. He is making an argument against purposeless accumulation — against working harder, longer, and more stressfully than you want to, in pursuit of a lifestyle you could design more simply right now.

The deepest insight in the parable is not the circular logic of the businessman’s plan. It is the fisherman’s clarity about what his life is for — and his confidence in that clarity. He knows what enough looks like. He is already living it. And no amount of sophisticated financial planning can improve on that.

Most of us are somewhere in between. We are not already living our ideal life, but we are also not clear on what that life actually requires. We have a vague sense that more money would make it better, without having done the specific work of defining how much more, and what for.

The Mexican fisherman’s real gift is not the punchline. It is the challenge embedded in the story:

Do you know what your enough looks like?

If you do — really, specifically, with real numbers — then you have something most people never build: a finish line. A target you’re actually aiming at, rather than a horizon that keeps retreating as you approach it.

If you don’t — if your answer to “how much is enough?” is “more” or “I’m not sure” or “probably more than I have now” — then the fisherman’s story is not a feel-good parable about simple living.

It is a diagnosis.

One Exercise to Do Before the End of the Week

Sit down with a pen and paper — not a spreadsheet, not an app, a physical pen and paper — and answer this question:

If I never had to work for money again starting tomorrow, what would my life look like? What would I do? Where would I live? How much would that life actually cost per year?

Write a specific annual number. Multiply it by 25. That is your freedom number.

Now look at your current net worth. Calculate the gap.

The gap is not a source of shame. It is a map. It tells you exactly where you are, exactly where the finish line is, and — combined with your savings rate — roughly how long the journey will take.

The fisherman already did this exercise. He just did it without a spreadsheet.

Disclaimer: This article is for educational and entertainment purposes. The 4% rule and savings rate projections referenced are based on historical data and are not guarantees of future results. Individual financial situations vary significantly. Consult a qualified financial professional before making major financial decisions.

Related reading:

- The Shockingly Simple Math Behind Early Retirement

- The 4% Rule: How Much Do You Actually Need to Retire?

- The Hedonic Treadmill: Why You’ll Never Feel Rich Enough

Leave a Reply